8-Week Green: Corporate Reality Overcomes Consumer Fears

By Fauzia Timberlake,

professional options trading coach

May 25, 2026

Market Roundup & The Week in Review

Despite dealing with a shaky start to the week, spiking bond yields, and an ongoing geopolitical overhang, the bulls stepped right back in mid-week. By Friday's close on May 22nd, the S&P 500 secured its eighth consecutive winning week—its longest sustained weekly rally since late 2023.

The big story of the week was the divergence between the hard market data and consumer reality. While the University of Michigan's consumer sentiment reading plummeted to a record low of 44.8 due to inflation concerns, corporate America sang a completely different tune. A stellar showing of Q1 earnings wrap-ups (including blowout figures showing the Magnificent Seven averaging 63% earnings growth) proved that corporate balance sheets remain remarkably robust.

Yield volatility did its best to derail the momentum early on, with the 30-year Treasury yield hitting a multi-year high of 5.18% on Tuesday before cooling off. Once long-term yields pulled back later in the week and crude oil eased down below $100 a barrel, equities found their footing, sparking a broad rally into the long Memorial Day holiday weekend. Notably, the Dow Jones Industrial Average eclipsed its historic peak, setting a fresh all-time record close on Friday.

Minutes from the latest Federal Reserve meeting released on Wednesday revealed policymakers are prepared to keep rates steady longer than expected—and even hinted at hikes if inflation refuses to behave. However, the market largely brushed this off, choosing to focus on stabilizing yields.

U.S. crude oil experienced a volatile ride, climbing above $108 a barrel early in the week before sliding back to around $97. This pullback relieved considerable pressure on inflation expectations and gave equity buyers the green light.

Strategy Corner

Based on this week's market movements, here are some trading ideas and option strategies for the readers' consideration. The positions can be scaled bigger (or smaller) to suit individual account size.

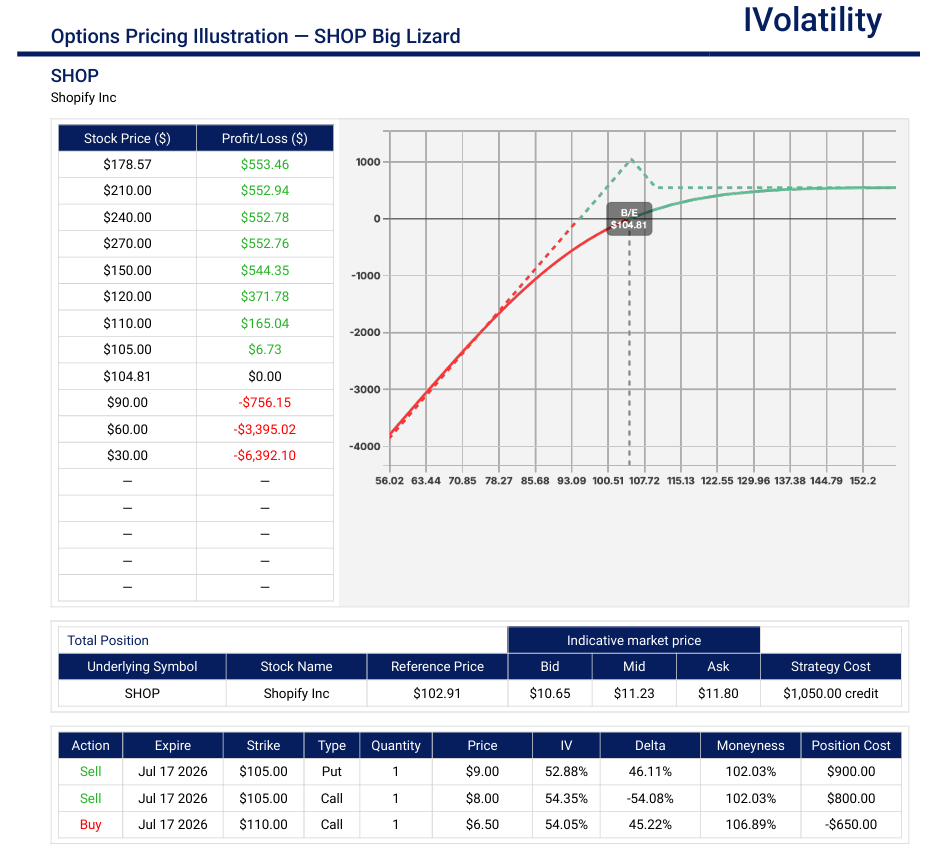

SHOP (closed at 102.99 on Friday, May 22nd)

Outlook: SHOP has taken a massive haircut recently—falling from around $127 down to a brief dip below $95 post-earnings before stabilizing this week. SHOP actually beat Q1 earnings expectations but shares were hammered because Q2 revenue guidance signaled a slight deceleration into the "high-twenties" percentage range.The selling pressure has largely exhausted itself, and institutional money may be sniffing around again.

Strategy: Big Lizard

In the July monthly expiration, sell the ATM $105 straddle and buy the 110call.

Premium collected about $1150 (enough to remove all upside risk by covering the $5 wide short call spread)

Downside breakeven around 93.50 (105-11.50) which is around 22delta

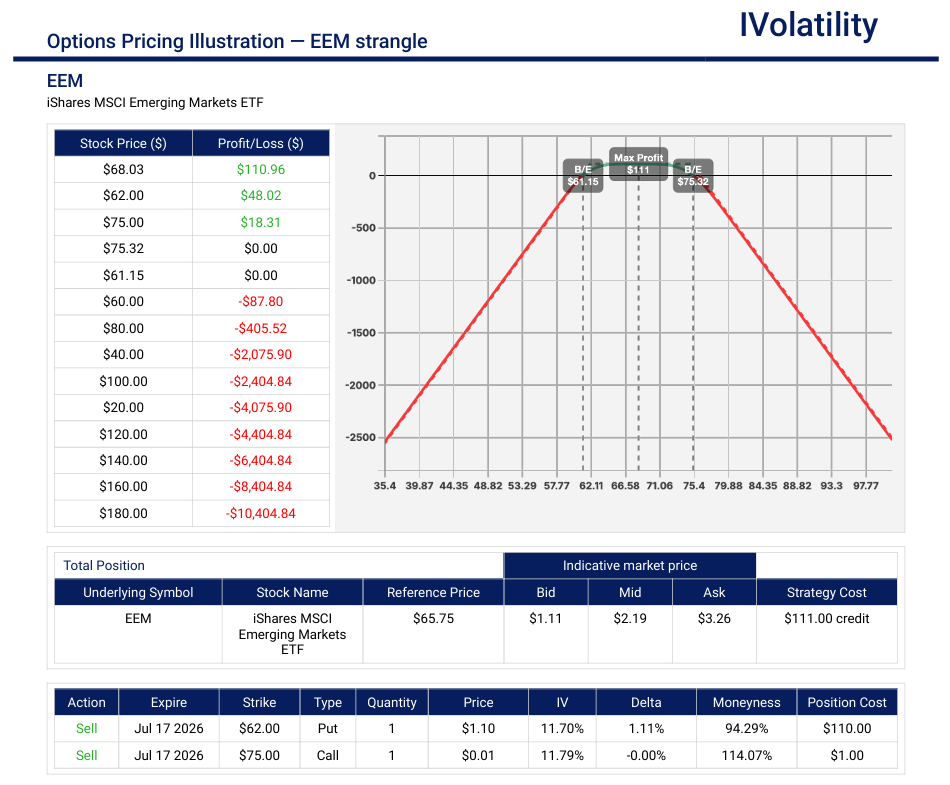

EEM (closed at 65.87 on Friday, May 22nd)

Outlook: after testing its 52-week high earlier in May near $68, EEM appears to be currently in a consolidation phase, making it a text-book candidate for range-bound strategies.

Strategy: Short Strangle

In the July monthly expiration, sell the 62put and the 75call.

Credit collected about $220

Net position delta about +20

Breakevens around 60 and 77

Movement of the Major Market Indices:

| INDEX | UP | DOWN |

| SPY | 0.78% | |

| QQQ | 0.84% | |

| IWM | 2.27% | |

| DIA | 2.13% | |

| GLD | -1.37% | |

| BTC/USD | -2.36% | |

| 10-year yield | -1.08% | |

| Crude Oil | -3.24% | |

| VIX | -9.68% |

Movement of the Major Market Sectors:

| SECTOR | UP | DOWN |

| TECH (XLK) | 1.56% | |

| FINANCIALS (XL) | 1.76% | |

| INDUSTRIALS (XLI) | 0.12% | |

| ENERGY XLE | 0.29% | |

| HEALTHCARE (XLV) | 3.30% | |

| UTILITIES (XLU) | 3.37% | |

| MATERIALS (XLB) | -0.08% | |

| REAL ESTATE (XLRE) | 2.93% | |

| CONSUMER STAPLES (XLP) | 0.06% | |

| CONSUMER DISCRETIONARY (XLY) | 2.30% |

Notable gainers for the week of May 18th – May 22nd

The trading week was defined by an interesting structural split: while the major indexes like the S&P 500 and Nasdaq-100 ground out modest gains, small-caps (IWM) surged over 2%. Under the surface, a massive rotation favored quantum computing, specialized semiconductor architecture, and select mid-cap tech players.

- Quantum Cyber N.V. (QUCY) soared up 315%. The stock exploded higher following news that the company secured an exclusive autonomous drone platform contract, a development heavily amplified by defense sector speculation as the Trump administration seeks a $55 billion budget allocation for drone warfare. Former VA Secretary Peter O'Rourke Sr. also joined the board.

- HCW Biologics Inc. (HCWB) flew up 262% after reporting better-than-expected Q1 2026 financial results alongside highly positive structural updates regarding its clinical pipelines and regulatory milestones.

- P3 Health Partners Inc. (PIII) jumped up 170% following the company's standout Q1 2026 financial results, revealing significant improvements in medical margin expansion and a sharp trajectory toward operational profitability, prompting strong institutional accumulation.

- Innodata Inc. (INOD) rallied sharply over 80% after reporting record-breaking Q1 2026 earnings, heavily driven by massive contract expansions with Big Tech enterprise customers needing large-scale AI data formatting.

- Arm Holdings plc (ARM) popped over 45%, leading the broader chip sector's late-week resurgence. Institutional buying intensified as the semiconductor sector broadened its appetite out of Nvidia and into architecture licensing winners, driving ARM past the major $300 milestone on heavy volume.

- Ross Stores, Inc. (ROST) rallied nearly 12% after reporting a significant Q1 earnings beat, expanding its operating margins, and explicitly raising its full-year sales and earnings guidance despite cautious broader retail sentiment.

Notable losers for the week of May 18th – May 22nd

While the broader equity indices pushed into positive territory by Friday's closing bell, under-the-surface sector damage was heavily concentrated in companies facing sudden restructuring announcements, disappointing updates to pivotal clinical trials, and downward earnings shifts.

- enGene Therapeutics Inc. (ENGN) dropped over 80%, suffering a massive sell-off after the company released updated interim results from its LEGEND pivotal cohort study. The fresh clinical data failed to meet the market's high efficacy expectations, triggering a rapid unwinding of speculative biotech positions.

- GD Culture Group Limited (GDC) shed nearly 80% after shares collapsed following the formal announcement that the company had established a special committee to evaluate a preliminary, non-binding "going-private" proposal. The terms of the potential buyout heavily disappointed public shareholders, causing a sharp downward re-pricing.

- Bitcoin Depot Inc. (BTM) shed over 73%. The crypto-utility provider capitulated after officially initiating a voluntary Chapter 11 bankruptcy process. The restructuring filing is intended to facilitate an orderly wind-down and a sale of the company's operational assets, deeply bruising equity holders.

- Entrada Therapeutics, Inc. (TRDA) dropped nearly 60%, gapping down severely on the heels of its first-quarter financial results paired with mixed topline data from Cohort 1 of its Phase 1/2 ELEVATE study evaluating ENTR-601-44 in patients with Duchenne Muscular Dystrophy.

- Intuit Inc. (INTU) shed over 18%. Serving as the heaviest institutional drag on the large-cap software space for the week, Intuit faced aggressive selling pressure as analysts digested its forward margin outlook and tax-season retention metrics, making it the worst-performing large-cap component over the five-day stretch.

- Ideal Power Inc. (IPWR) dropped over 16%, despite recently publicizing its structural involvement with a key partner inside NVIDIA's Rubin Ultra 800V DC AI data center ecosystem, the stock experienced a classic "sell-the-news" event, with aggressive profit-taking and short-seller accumulation driving shares down from their recent highs.

Review selected market indices below:

Daily Notable Market Action

Monday's Markets and News:

U.S. equity markets pulled back modestly on Monday as bond yields extended their recent upward trajectory. The S&P 500 hovered near unchanged, finishing slightly in the red, while tech-heavy growth spaces saw a bit more pressure.

Energy led the day's gains, heavily supported by rising oil prices as geopolitical disruptions persisted in the Strait of Hormuz.

Technology & Industrials lagged behind, absorbing the pressure from escalating fixed-income yields.

Treasury yields continued their march higher on Monday, pulling capital out of high-multiple growth equities.

WTI Crude traded higher amid ongoing Middle East supply anxieties, providing a strong tailwind for energy producers.

U.S. Dollar eased back slightly against a broad basket of currencies, cooling off after logging a highly robust performance the prior week.

- S&P 500: 7,403.05 (-0.1%)

- Nasdaq: 26,090.73 (-0.5%)

Tuesday's Markets and News:

U.S. equities extended their slide for a second consecutive session as inflation and geopolitical uncertainties kept market participants on the defensive. Heightened anxieties surrounding the ongoing Middle East conflict and multi-month highs in Treasury yields triggered a broader rotation out of highly valued growth areas and into defensive allocations.

The technology sector faced heavy profit-taking ahead of highly anticipated corporate earnings from market heavyweights. Market strategists noted a distinct shift toward harvesting massive year-to-date AI and tech gains to shore up more stable, deep-value sectors.

Crude oil prices hovered persistently above $108 a barrel. The tandem rise in both fuel costs and bond yields began weighing heavily on consumer discretionary spaces, as analysts flagged early signs of cooling consumer confidence.

The 10-year Treasury yield surged to a 16-month high of 4.70%, on growing concerns that sticky, conflict-driven inflation could force the Federal Reserve to hold interest rates steady far longer than Wall Street anticipated.

- S&P 500: 7,354.00 (-0.67%)

- Nasdaq: 25,871.00 (-0.84%)

Wednesday's Markets and News:

Wall Street snapped its three-day losing streak in dramatic fashion, roaring back to within striking distance of all-time highs. A sudden wave of geopolitical optimism and a massive corporate earnings victory late in the day completely reversed the week's negative momentum.

Markets gapped higher on news that the U.S. and Iran reached a tentative "letter of intent" to pursue 30 days of de-escalation negotiations. While unresolved friction points remain, the headline sent a massive sigh of relief through global markets.

In response to the diplomatic progress, global energy pressures eased rapidly. Brent crude tumbled 5.6% back toward $101 a barrel, allowing the 10-year Treasury yield to recede back under 4.60%. Rate-sensitive growth, retail, airline, and homebuilder equities aggressively rebounded.

- S&P 500: 7,432.97 (+1.08%)

- Nasdaq: 26,270.36 (+1.54%)

Thursday's Markets and News:

Equities experienced a choppy, volatile session on Thursday, staging a midday turnaround to finish slightly positive. Investors spent the day digesting massive cross-currents, balancing blow-out tech earnings against fresh friction in oil and bond markets.

Industrials and specialized tech received a powerful tailwind following news that the administration is distributing $2 billion in federal quantum-computing grants. IBM climbed over 6% on plans to establish a government-backed quantum foundry, lifting several peers in the sector.

Despite solid earnings, market reactions were heavily fragmented. Retail titan Walmart (WMT) fell 2% on cautious forward guidance linked to fuel costs, while Intuit (INTU) plunged 14% on weaker TurboTax metrics and announced 17% workforce reduction.

Markets opened in the red after rhetoric out of Tehran regarding uranium enrichment temporarily pushed Brent crude back near $109 a barrel. However, energy prices reversed course during midday trading, sliding back down toward $102, which instantly pulled Treasury yields lower and sparked an afternoon equity rally.

- S&P 500: 7,447.80 (+0.20%)

- Nasdaq: 26,322.90 (+0.20%)

Friday's Markets and News:

U.S. equities rallied broadly, wrapping up an eighth consecutive winning week—the longest sustained positive streak for Wall Street since late 2023. Despite starkly contrasting consumer data matching historic lows, institutional buying pushed the blue-chip Dow Jones Industrial Average to a fresh record high ahead of the three-day holiday weekend.

The University of Michigan's final May Consumer Sentiment Index fell significantly to 44.8, piercing below the previous historical trough set in June 2022. Driven by anxieties over sticky fuel prices and the ongoing war with Iran, 57% of surveyed households explicitly noted high prices are actively eroding their personal finances. Yet, a record influx of M2 money supply and robust corporate earnings growth kept equity demand exceptionally aggressive.

Strong corporate reports continued to anchor market optimism. Off-price retail leader Ross Stores (ROST) jumped 8.1% on robust foot traffic, while software mainstays Workday (WDAY) climbed 5.2% and Zoom Communications (ZM) surged 9.2% after both cleared Q1 profit expectations with ease.

Ahead of the Memorial Day closing, the 10-year Treasury yield settled lower near 4.57%. WTI Crude oil prices stabilized sideways to finish around $97 per barrel, cooling down as market participants digested early diplomatic headlines from the mid-week de-escalation talks.

- S&P 500: 7,473.47 (+27.75 / +0.37%)

- Nasdaq: 26,343.97 (+50.87 / +0.19%)

- DJIA: 50,579.70 (+294.04 / +0.58%)

Notable Earnings (May 25th – May 29th)

Wednesday afternoon is a massive catalyst for tech investors. CRM and SNOW will offer critical commentary on enterprise software spending and how cloud allocations are shifting, while MRVL serves as a key hardware demand indicator for data infrastructure.

Following a bumpy road for retail discretionary spending earlier in May, results from COST, BBY and DG on Thursday will provide a definitive cross-section look at how varying inflation pressures are impacting high-, mid-, and low-tier household spending habits.

The actual earnings date may vary, so traders should confirm with their brokers. If a trader wishes to open a position to participate in earnings announcements, it is important to check whether the earnings are released BEFORE the markets open or AFTER the markets close on the date of earnings.

Monday, May 25th: markets will be closed for Memorial Day holiday

Tuesday, May 26th: AZO / A

Wednesday, May 27th: ANF / DKS / CRM / HPQ / SNOW / MRVL / SNPS

Thursday, May 28th: BBY / BURL / DG / COST / PATH / DELL/ GPS

Friday, May 29th: no notable earnings reports on deck

Economic Calendar (May 25th – May 29th)

Tuesday morning's Conference Board Consumer Confidence reading will give a real-time check on how high fuel costs (with crude oil hovering above $100 a barrel) are weighing on household psychological expectations. Look for the "Expectations Index" sub-component to tell you if a broader retail slowdown is brewing.

Thursday at 8:30 AM ET may present significant market volatility. Traders are focusing on the Core PCE Price Index, the Fed's absolute favorite metric for evaluating inflation trends because it shifts along with consumer spending adjustments. If the year-over-year figure stays sticky or pops higher than the 3.2% consensus, expectations for a near-term interest rate cut will get pushed back out.

GDP Revision Verification: Dropping simultaneously with inflation is the second estimate for Q1 GDP growth. The initial flash reading came in sluggish at 0.5%. Wall Street economists are widely projecting a major upward revision toward 2.0% based on cleaner retail and services data collected later in the quarter. A strong upward revision signals economic resilience but may give the Federal Reserve more room to keep rates "higher for longer."

- Monday, May 25th:

Markets closed for the Memorial Day holiday - Tuesday, May 26th:

Chicago Fed National Activity Index

S&P/Case-Shiller Home Price Index (YoY)

CB Consumer Confidence - Wednesday, May 27th:

MBA Mortgage ApplicationsWeekly

Richmond Fed Manufacturing Index - Thursday, May 28th:

Core PCE Price Index (MoM)

Core PCE Price Index (YoY)

GDP Growth Rate (2nd Estimate)

Initial Jobless ClaimsWeekly

Personal Income / Personal Spending

Durable Goods Orders - Friday, May 29th:

No major U.S. macroeconomic data scheduled

Blue Sky Horizons

The Great Migration to the Edge

For the past three years, the market's obsession with artificial intelligence has been entirely focused on the Cloud—the multi-billion-dollar data centers packed with thousands of liquid-cooled graphics processors (GPUs) running massive, power-hungry models. Hyper-scalers have poured record-breaking capital expenditures into building these centralized data fortresses.

But looking past the current earnings cycle to the next 5 to 10 years, a massive structural shift is quietly underway. The future of computational value isn't just about building bigger clouds; it's about migrating intelligence directly to the Edge.

In technology terms, "the edge" refers to processing data physically close to where it is actually generated, rather than routing it back and forth to a distant, centralized cloud server. Think of the smartphone, an autonomous vehicle, a smart medical device, or an automated robotic arm on a factory floor.

Moving intelligence to the edge solves the three structural bottlenecks currently challenging the scalability of the digital economy:

- Latency: For an autonomous vehicle traveling at 65 mph, a 100-millisecond delay spent waiting for a cloud server to identify an obstacle is the difference between safety and disaster. The edge allows for split-second, localized decision-making.

- The Power & Infrastructure Wall: Centralized data centers are consuming an unsustainable amount of the global electrical grid. The future relies on highly dense, task-specific Small Language Models (SLMs) that require a fraction of the compute and can live entirely on-device.

- The Privacy Stack: In an era of strict data compliance and intellectual property security, enterprise clients and healthcare providers are increasingly hesitant to ship sensitive proprietary data or patient records to third-party clouds. Edge computing allows data to be processed and discarded locally.

Major Wall Street research indicates a move towards an "Agentic Economy" where autonomous software agents will handle everything from supply chain remediation to cell phone navigation. Goldman Sachs recently projected that as consumers and enterprises adopt these goal-driven autonomous systems, global token consumption (the computational units used by AI models) will multiply an astonishing 24 times between 2026 and 2030. Running that volume of data entirely through traditional cloud architecture would completely break the internet's bandwidth and power infrastructure.

As the technological landscape matures, a dramatic dispersion in hardware and software leadership might be seen emerging. The initial phase of the tech boom rewarded the raw computing power of the cloud. The next phase will reward the companies mastering efficiency: semiconductor designers developing ultra-low-power edge architectures, device manufacturers integrating localized neural processing units, and enterprise software giants deploying nimble, specialized edge agents.

The cloud built the foundation of modern intelligence, but the edge is where it will actually live, work, and scale.

Thank you for reading. Until next week's close,

Safe Trading!

Fauzia Timberlake

About the Author: Fauzia Timberlake is a professional options coach and financial strategist specializing in risk management and portfolio architecture for self-directed investors.

Questions / Comments

We're here to serve IVolatility users and we welcome your questions or feedback about the option strategies discussed in this newsletter. If there is something you would like us to address, we're always open to your suggestions. Use support@ivolatility.com.

Previous issues are located under the Trade Ideas tab on our website.